How do these Payday loans work?

Contents

The following scenario is an example of a typical payday and auto title loan transaction and demonstrates how they can lead to serious trouble.

Let’s say that a single mother is in need of a $300 loan and goes to a payday lender because she has a poor credit history and no credit card. She writes a post-dated check to a payday lender for $361.06 ($300 principal loan, plus $1.06 interest, and a $60.00 service fee). The payday lender promises to hold the check for two weeks until she gets paid again.

The next payday, after the due date, she will either pay off the full amount of $361.06 or if she is unable to, she is left with two options. It is important to realize that she cannot pay off the loan in installments; she must pay it in full. If she cannot, she could default on the loan and the payday lender will then cash the check. The check will bounce incurring penalty fees from both the bank and the lender.

Or, in order to avoid the penalties, she pays the $60.00 fee again and the loan “rolls over.” This fee simply gives her two more weeks to pay the entire original amount; it does not reduce the amount she must pay all at once. The rollover fee must be paid every two weeks if she cannot pay off the full amount. The fee never reduces the balance of the loan and there is no limit to the number of times the loan can be rolled over. If the loan was paid off after just one rollover, a month after she initially borrowed the money, a $300 loan would cost $421.06. That’s $121.06 in fees and interest in four weeks.

Auto title loans are similar but are much more dangerous because the principal borrowed and the fees charged are much higher. Instead of a check, a borrower uses their car title as collateral. They then borrow an amount of money that is only as high as 40 – 50% of the value of the car. For example, if a borrower owned a car worth $10,000 they could borrow about $4,000. Like payday loans, the entire amount of the loan plus interest and fee is due at once, but typically at the end of a one-month term, not two weeks.

The fees and interest on a $4,000 loan can be as high as $1,200. That means that a borrower can pay $1,200 a month repeatedly and never reduce the balance of the loan. In just four months this $4,000 loan can cost the borrower nearly $9,000.00. If the borrower defaults, their car is repossessed and sold to pay off the loan.

How is this legal?

The Texas Constitution grants the legislature the authority to define interest and to fix maximum rates. It also states that in absence of legislation, all contracts with an interest rate greater than 10% shall be deemed usurious.

Payday and vehicle title lenders, on the other hand, do not operate as lenders authorized by the Texas Finance Code, as one might anticipate. Instead, they used a loophole in the Credit Services Organizations (CSO) Act, which places no restrictions on the interest rates and fees they charge borrowers.

The CSO Act was adopted in 1997 and is intended to control how credit restoration firms might assist persons attempting to restore their credit. This legislation empowers CSOs to “seek an extension of consumer credit for a customer.” The intention is clear: CSOs will be permitted to assist Texans with negative credit in building a good loan history in order to improve credit ratings. Instead, over 98% of the state’s licensed CSOs are payday and auto title lenders that do nothing except hurt people’s credit.

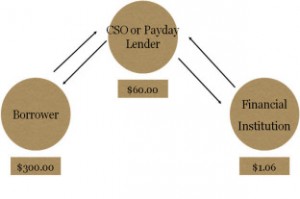

In practice, payday and vehicle title lenders are essentially credit brokers or arrangers. They collaborate with banks or other major lenders who offer interest rates lower than the 10% APR constitutional limit, whilst the payday lender, registered as a CSO, imposes outrageous fees. This figure depicts the link better –

The actual lender, the financial institution, charges a low-interest rate and makes a modest profit on the brief loan. The loan is arranged, collected, and guaranteed by the CSO for a significant fee. This is usually roughly $20 for every $100 borrowed, although there is no legal limit. The borrower is never in contact with the lender.

The CSO loophole is only the latest trick payday and auto title lenders have used to evade Texas lending laws.

In 2001 the Texas legislature created Texas Finance Code Section 342.007 “DEFERRED PRESENTMENT TRANSACTION” in order to govern payday lending in this state. The code contains a rate and fee schedule which limits these and many other consumer loans. However, payday and auto title lenders in Texas discovered that they could avoid these rates and fees by partnering with out-of-state banks to serve as loan originators. This scheme became known as the Rent-A-Bank model. Fortunately, in 2005 the FDIC closed this loophole by prohibiting this relationship. It is at this time that the CSO loophole, created in 1997, became widely utilized.

The Big Problem in Texas

This wide-open loophole has enabled an explosion of payday and auto title lending in this state. A registered CSO must only file with the Secretary of State, pay a $100 registration fee, no matter how many locations they operate, and then list their locations.

In 2006 there were 1,279 CSOs registered in Texas.

In 2010 there are over 3,594 registered in Texas.

That’s more locations than Mcdonald’s and Whataburger combined.

Our lack of regulation means that Texas payday and auto title loans are the most expensive loans in the country.

The Texas Office of Consumer Credit Commissioner does not have any regulatory power over CSOs like other consumer lenders. The Attorney General has been unresponsive to complaints. Therefore, there is no agency that both takes consumer complaints and helps to resolve disputes.

Alternatives are Available

Payday and auto title loans are not the only place to turn for people who find themselves in a financial crisis. They market themselves as the quickest and easiest option, but the price for such convenience is clearly too high for Texas families. In order to avoid these high-cost loans, people need to know that alternatives are available, even to people with poor or no credit history.

In particular, many credit unions are stepping up to provide alternative small-dollar loan products. In September of 2010, the National Credit Union Administration launched a program that combats these unfair practices by offering similar loans at better terms for borrowers. The new rules contain many consumer protections yet also ensure that making the loans will be cost-effective for credit unions. Small-dollar loans offered by national credit unions will have interest rates no greater than 28%, application fees under $20, will limit the number of loans that can be made to one person, and limit the number of times the term can be extended or “rolled over.”

In Texas, the Texas Credit Union Department also recently changed its rules to allow more flexibility in short-term lending practices. With new regulations similar to those established nationally, Texans can be sure that local credit unions will not participate in predatory practices, and will instead be part of the solution.

It is quite possible that big, traditional lenders and banks will soon be providing more small-dollar loan alternatives. Recently, the FDIC completed a two-year pilot study that included 28 banks from 15 different states that made more than 34,400 small-dollar loans. The result was a “Safe, Affordable, and Feasible Template for Small-Dollar Loans” that established many new long-term, profitable relationships with customers. For more complete information about the pilot program see the link in our resource section.

Another option available is to request an advance from an employer, many are willing to offer them. Even cash advances on credit cards, for those that have them, offer better rates than payday and auto title lenders.

Our communities of faith are also often a source of funds in emergency situations.

The Center for Responsible Lending has a more complete list of alternatives that can be found in our resource section.

Why We Care

This practice hurts Texas families. Money spent on rollover fees is not spent on necessities. Paying these fees may leave some in a position where they must seek government assistance or turn to congregations or others providing aid. Fees paid to service these loans rob our state because they are not subject to sales taxes and instead siphon off money that would otherwise be spent on goods that would generate sales tax revenue. We refuse to stand by any longer while our fellow citizens are lured into an unregulated debt trap with the promise of quick cash.

Additional Resources: